Big Life Events

Buying a home, car, or even furniture with credit are all considered big life events. Know your credit report and credit score. There are three major nationwide consumer reporting companies: Equifax, TransUnion, and Experian. But, they aren’t the only companies that collect information on you. There are others, and all of the bigger nationwide companies must provide a free report no less than once within a 12-month period. But, in response to the Coronavirus (COVID-19) pandemic, you can request your credit reports for free weekly from each of the these companies through December 2023. This is due to pandemic related scams. Ouch! As sad it is, it’s true. I’ve put together some info and resources on these pandemic scams, what to watch for, and how to report them. Go to my post, Guard Yourself From Pandemic Scams to learn more.

Reasons to Request Your Information

Your credit score and buying a home, car, or even furniture with credit are a big deal in the credit world. Knowing your credit report and credit score is important at this stage. It’s best to check your personal information with these companies to make sure they are accurate, if you intend to rent, buy a home or car with credit, or otherwise intend to apply for credit in the near future.

When to Check Credit Reports

Your Personal Information

Your personal information is gathered, and saved by companies like Equifax, TransUnion, Experian, and SageStream. SageStream, LLC is now part of LexisNexis® Risk Solutions is one of the companies that provides consumer reports to different types of companies including credit card issuers, retailers, and wireless telephone service providers. You can request a credit report to verify the information they have about you. To obtain your credit report from each of the three major nationwide consumer reporting companies: Equifax, TransUnion, and Experian, go to annualcreditreport.com

Once you receive your report, review it carefully, and dispute suspected discrepancies.

1. Request

2. Review

3. Dispute

After reviewing your report, and it looks accurate, you are on your way! Next step, see what improvements you can make. I talk about those improvements in this post. If you have reviewed it, and have found inaccuracies, discrepancies and/or fraud, read my post, Credit Reports and Identity Theft for your next steps.

What Is Credit?

Credit is the ability to borrow or access, goods or services with the understanding that you’ll pay back later. Lenders merchants, and service providers, known collectively as creditors, grant credit based on their confidence that you can be trusted to pay back what you borrowed. Along with any finance charges that may apply to the extent that creditors can consider you worthy of their trust, you are said to be credit, worthy or to have a good credit.

3 Types of Credit

1. Revolving credit

2. Installment credit

3. Open credit or service credit

Revolving Credit

With revolving credit, you are given a maximum credit limit, and you can make charges each month. You carry a balance of the debt and make a payment. Most credit cards are a form of revolving credit.

Installment Credit

Installment credit is a loan for a specific sum of money you agree to repay plus interest and fees in a series of equal monthly payments. Student loans, car loans, mortgages are all examples of installment credit.

Open Credit or Service Credit

Open credit or service credit involving a utilities account for gas, electric, or water are all good examples of open credit. The amount you owe each month will vary depending on how much of the commodity you actually use and the entire balance is expected to be paid each month.

Your Credit History

Credit history is summarized in files, known as credit reports. These credit reports are compiled by three independent credit bureaus: Experian, Trans Union, and Equifax. Banks and credit unions voluntarily report re-payment information to the credit bureaus. The info will include your identifying information such as your name, address and phone numbers, public records, such as bankruptcy, monetary judgments, tax liens, and child support, and lastly, credit information and inquiries, which include creditors and collections.

Credit Scores

Credit scores range from 350 to 850. In real estate, there are less that will borrow to individuals with a score of 580. The Fico score focuses on the last 12 to 24 months of payment history. So, it is possible to rebuild your credit, if it’s necessary.

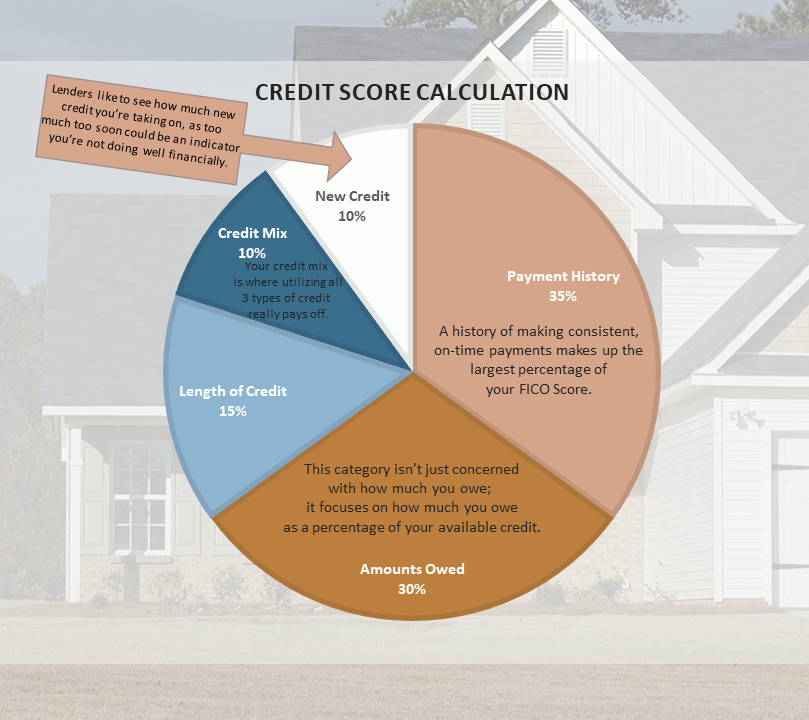

How Scores are Calculated

Scores are calculated by the following percentages 35% of your Fico score is built upon payment history. Credit history is also made up of making consistent on-time payments. This is the largest percentage of your Fico score. Thirty percent is based on the amount that you owe. This category is it focused on how much you owe as a percentage of your available credit. The length of credit or how many years you’ve had credit equals 15%. And, 10% is the mix of credit. It shows how you are utilizing all 3 types of credit. And lastly, lenders like to see how much new credit you are taking on. If it shows too much too soon, it could be an indicator that you’re not doing well financially. This makes up 10% of your credit history.

Soft and Hard Inquiries

An inquiry is an attempt to acquire credit. Hard inquiries occur when a lender requests your credit report when you apply for credit as part of the decision making process. This type of inquiry will influence your score. Too many hard inquiries in a short period of time can be concerning to lenders. Opening various new accounts show that you’re having trouble paying bills. Soft inquiries occur when you check your own credit or a credit card company checks your credit for pre-approval. These do not affect your credit score.

Lenders

In real estate, your lender will pull a tri-merge credit report that will merge all three credit companies and use the middle score. This is your Fico score.

Vantage Score VS FICO Score

A Vantage score is used if you’ve ever signed up for credit watching software, they use the vantage score and lenders use the Fico score. The general rule of thumb is to target a credit score of 620. A good credit score ranges between 670 and 739. A fair score ranges from 580 to 669. If you are pursuing the homebuying process, the first step is to be pre-approved by talking with a local lender. After pre-approval, talk to a real estate agent, such as myself. Reach me at jodytuckerrealtor@gmail.com

Rebuilding Your Credit

Rebuilding credit is a good decision if your score is less than 600. The first step is to order a credit report from each credit bureau. You have the right to get a free credit report annually. If you find errors or discrepancy, you can write dispute letters to the credit bureaus. As you continue to rebuild your credit, you can establish good credit by opening a credit card from a reputable company and pay it off each month. Paying off your existing debt and getting a receipt to submit to the credit bureaus to update your credit file is also very good to do.

Be Smart About Your Credit

Be smart about your credit! Pay on your debts, only borrow what you can repay, and never give your credit card over the phone unless you know who it is. Report lost or stolen cards promptly. Review your credit reports promptly. Keep your credit balance under 50% of the credit limit. Lastly, limit the amount of hard inquiries that you allow on your credit as they can really impact your score. Thank you so much for reading my today. I hope that you learned a lot about credit, and that it will help propel you into the homebuying process and in finding your dream home!

Contact Me!

If you live in the Duluth or surrounding areas, let’s chat about your plan to purchase a home. I would love to be your Realtor!

Jody Tucker, MN Licensed Realtor

Messina & Associates Real Estate, Inc.

218-349-1792

jodytuckerrealtor@gmail.com

![]()

Follow Me!